FX Daily Strategy: APAC, May 1st

FOMC the focus, Fed expected to be more hawkish

Risk may be to USD downside, as market already priced for hawkish shift

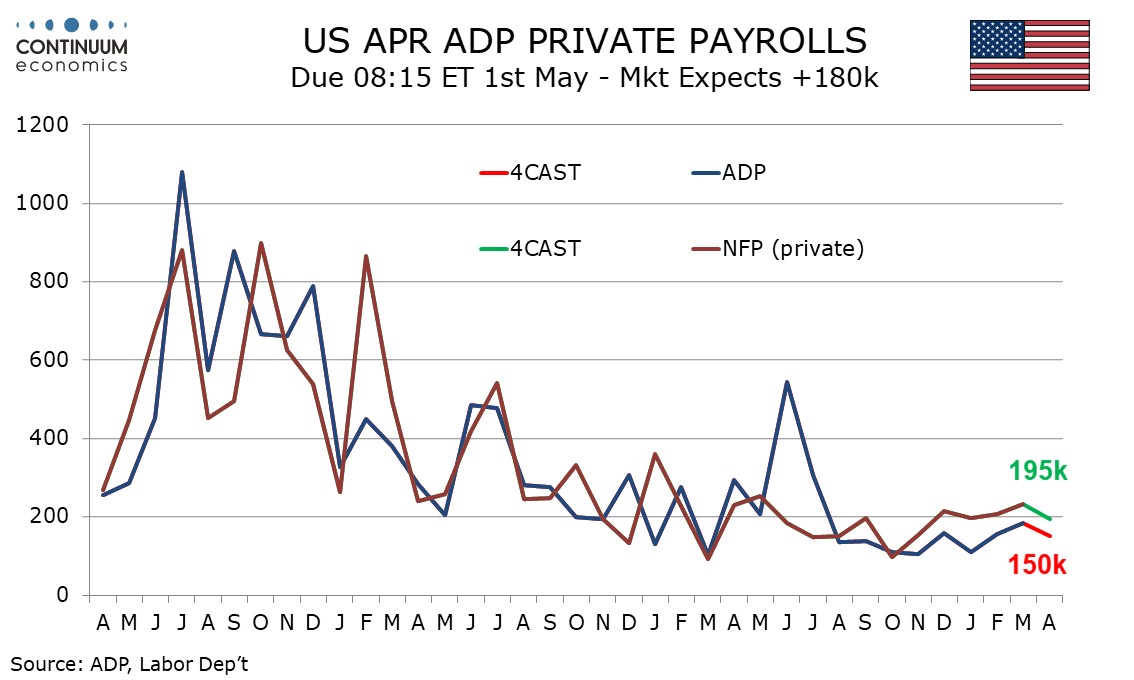

ADP unlikely to move markets

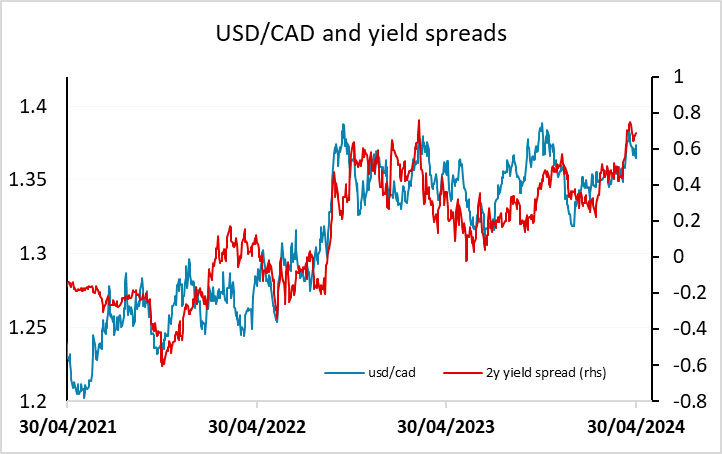

Macklem could impact the CAD

FOMC the focus, Fed expected to be more hawkish

Risk may be to USD downside, as market already priced for hawkish shift

ADP unlikely to move markets

Macklem could impact the CAD

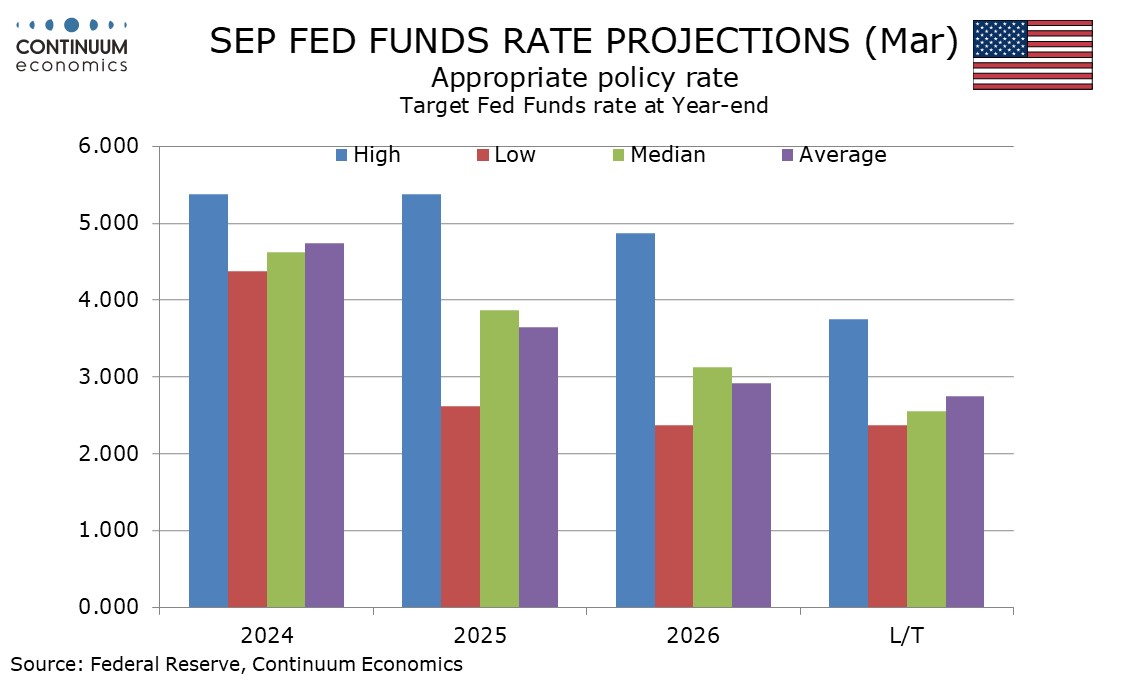

Wednesday’s focus will be on the FOMC meeting. Rates look sure to remain at the current 5.25%-5.50% target range, so market reaction will depend on changes to the statement and the tone of Powell’s press conference. The statement is likely to see some adjustments to reflect recent disappointment on inflation while repeating that more confidence on inflation moving towards target is needed before easing. It is also likely that tapering of Quantitative Tightening will be outlined at this meeting, but this should not be seen as a dovish policy signal.

In the January and March statements the key wording was that “the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%”. This looks unlikely to be changed, but the FOMC is likely want to signal even greater concern over inflation than was the case in March. The dots will not be updated at this meeting, but Chairman Powell is likely to be cautious about giving a message consistent with the March dots that saw rates being eased this year. He is likely to stress that the dots are not a plan but dependent on the evolution of data, and recent data suggests that easing is not yet appropriate. The dots will next be updated on June 12. March’s dots projected three 25bps easings in 2024 but only one participant needs to shift to leave the median at two. As it stands, the market is pricing in only 30bps of easing this year, so it looks like the Fed will need to be significantly hawkish for US yields to rise significantly in response to the statement. The risks may therefore be that the Fed is less hawkish than feared, in which case we could see yields and the USD drop in response.

Ahead of the FOMC there is ADP data which may have some influence on market expectations from Fridays employment report, but as we have seen in previous months, the ADP data is not necessarily a good guide to payrolls and the market will take the numbers with a large pinch of salt. We expect a 150k increase in April’s ADP estimate for private sector employment growth, which would be in line with recent trend, but we see this continuing to underperform private sector non-farm payrolls, which we expect to rise by 195k. We expect overall payrolls to rise by 255k.

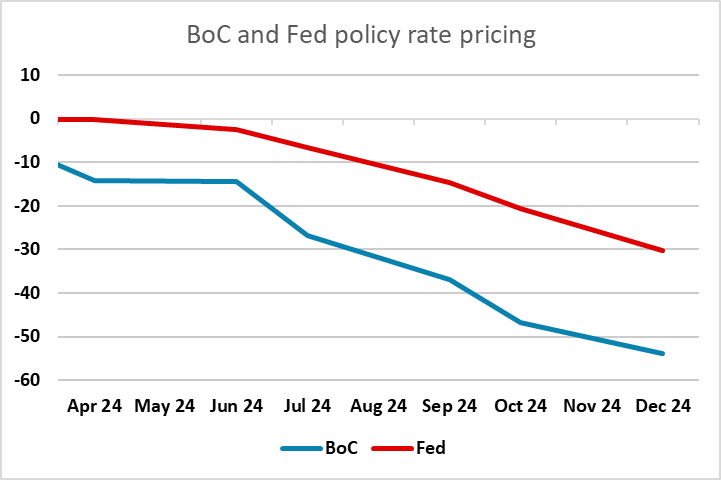

There is nothing happening in Europe, with most of the continent closed for the May Day holiday. The UK is open but there is nothing of interest on the UK calendar. There may be potential for some impact in Canada from speeches from governor Macklem. The February GDP data released Tuesday was slightly on the weak side of expectations, and the market is still very much divided on whether we will see a BoC rate cut in June. This is currently priced at slightly less than a 60% chance, so anything Macklem says could have a significant impact. As it stands USD/CAD looks to have some small potential to rise based on current spreads, but the CAD is likely to move in whichever direction Macklem points.